Digital Nomad Finance: Emerging Opportunities for Mobility-First FinTech

Digital nomads and mobile employees are exposing product gaps across banking, tax, insurance, payroll, and travel.

As work becomes increasingly location-independent, many people are exploring the possibilities of remote work, including digital nomading. With uncertainty about the state of the traditional job market persisting, Greenefield predicts that more people will experiment with freelance and location-independent work.

However, financial systems haven’t caught up. This is especially true for digital nomads. Facing challenges in banking, receiving and making payments, and managing budgets across borders, digital nomads effectively provide a stress test of today’s global fintech offerings.

This blog will explore opportunities in fintech and embedded finance to better serve the needs of digital nomads and other borderless workers.

Digital Nomads Expose Infrastructure Gaps

As of 2025, an estimated 40 million or more people participate in some form of digital nomading globally, including over 18 million US citizens.

Many nomads are in transportable freelance or contract roles as digital marketers, content creators, software developers, and remote teachers. However, there is an increasing population of entrepreneurs as well as individuals who work traditional jobs while nomading.

Downstream, digital nomads have inspired some who cannot commit to full-time traveling to other types of careers built upon remote work, location flexibility, and self-determination. Yet others have taken on more “workcations” abroad, operating similarly to a digital nomad for short bursts of time.

All of this has led to a sizable global, remote worker community with increasingly sophisticated needs in banking, financial services, and insurance. Their global nature creates unique requirements, risks, and opportunities – and may just be a leading indicator for the future of work.

The Core Problem: Financial Systems Built for Static Lives

Most financial products have historically assumed that the user has a static country of residence and operates in a single currency. There have been good reasons for this – banking and financial regulations differ across countries. Moreover, managing multiple currencies with varying stability adds complexity.

Digital nomads quickly learned where traditional financial systems and applications broke for them:

Banking tied to residency. Financial regulations in many countries mean strict requirements for where customers live and how they prove their residency. Nomadic workers without a permanent physical address have found their bank accounts abruptly shut down – with few avenues to establish a new one.

Payroll tied to local entities. Traditional models where payroll is run locally based on domestic, state/province, and municipal tax structures are going to run into problems when employing globally distributed workers. While there are ways to accommodate this, they are subject to friction from currency exchange, legal, and tax structures that may not be ideal for the worker.

Tax systems tied to jurisdiction. While digital nomad visas can provide some reprieve from multiple taxation, nomads working in multiple countries over the course of a year often find themselves dealing with a confusing cluster of forms and rules to deal with at tax time. Facing costly repercussions from the potential of honest oversights and mistakes, taxes can be a major obstacle to living the nomad dream.

Insurance tied to geography. Managing health, travel, and other types of insurance across jurisdictions can be confusing. Nomads can struggle to make sure that they have the appropriate insurances at the right level of coverage.

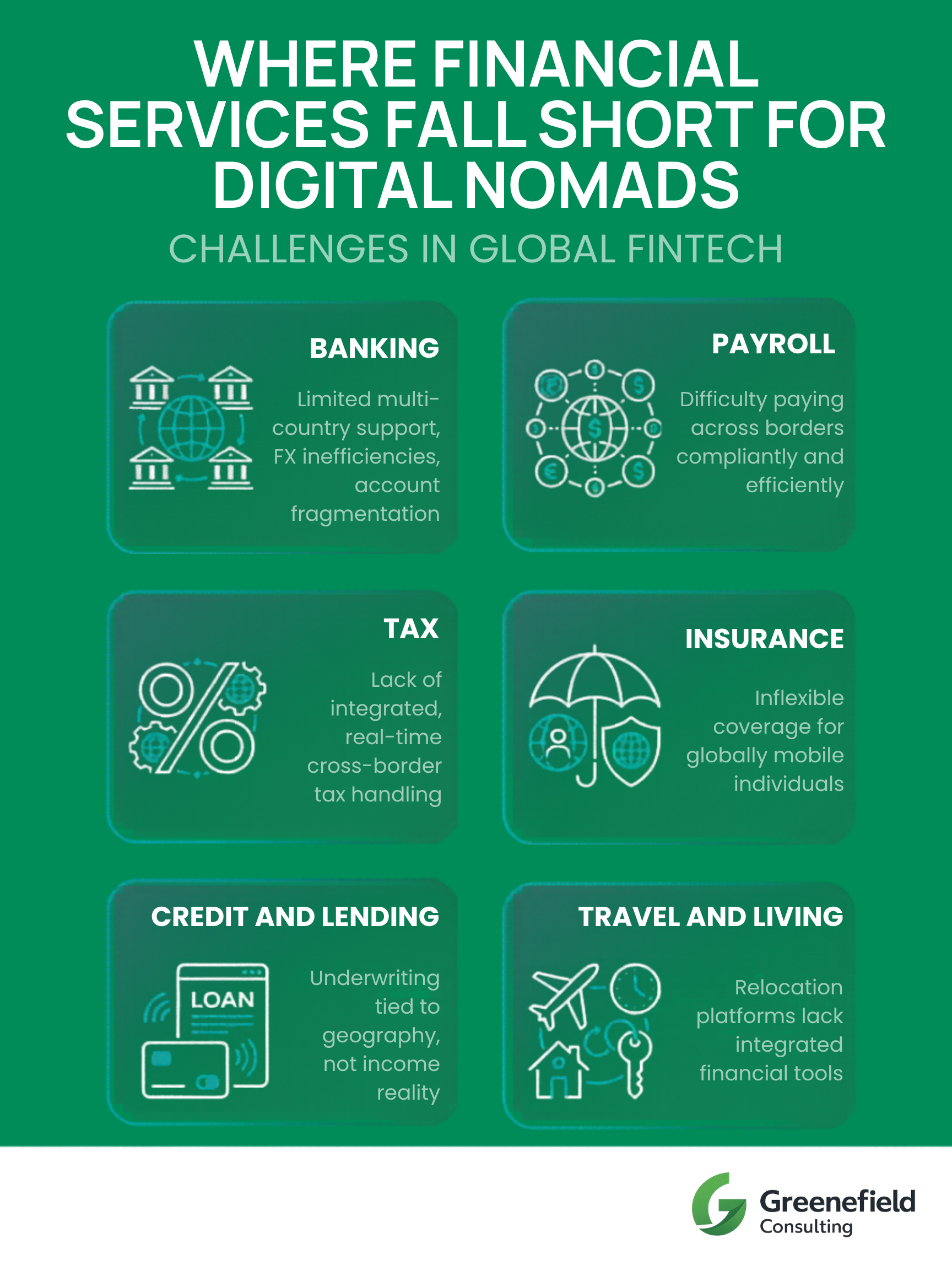

These are just a few examples of where traditional financial tools can fall short for digital nomads. The infographic below illustrates broader areas of friction.

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Where Financial Systems Fall Short for Digital Nomads

As you can see, the potential for friction exists in virtually every facet of financial life. If you follow r/digitalnomad on Reddit, you’ll occasionally see horror stories of individuals locked out of their bank accounts. Other common frustrations include dealing with currency exchange rates and fees and trouble with opening new bank accounts (personal or business) or lines of credit.

For those not going the entrepreneurial route, remaining employed in a traditional company becomes more tenuous as both employer and employee wrestle with tax and employment laws for traveling workers, and the resulting payroll obstacles. Similarly, this creates friction for digital nomad entrepreneurs as they navigate their need for additional workers when their businesses grow.

Insurance is another area where trouble can arise for nomads. Managing insurance requirements, availability, and claims across borders can lead to frustration for nomads, from the extra effort required to navigate cross-border insurance to the potential of finding out that you’re not covered at a precarious moment.

Even when nomads are able to sort out the fundamentals of their financial lives, they still often have to manage money in a fragmented way. A remote employee who spends time in multiple countries each year often ends up juggling several disconnected tools to manage income, taxes, insurance, and spending.

Vendor opportunity lies in integrating these components in one place, as well as pursuing integrations with travel planning and management.

The Rise of the Digital Nomad Finance Mobility Stack

A new generation of platforms is emerging to abstract away the operational complexity of borderless living and work.

The above image is a great high-level overview of the new financial mobility stack for digital nomads. Rapidly evolving areas in this space include:

Neobanks

Referring to digitally-native providers of app-based banking services, Neobanks have become commonplace. Well-known neobanks include Chime, SoFi, and Revolut. This rapidly evolving segment is estimated to serve 350 million users globally in 2026, having doubled in adoption over the last five years.

Wallets and Payments

Neobanks aren’t the only fintech providers helping digital nomads with payments and money management. Nomads also may rely on money transfer and multi-currency apps such as Wise. Companies such as GrabrFi have emerged to help those who need an account with a US-based identity.

Employer of Record Platforms

For companies that want to enable employees to work as digital nomads, Employer of Record (EOR) software facilitates creating a legal entity in a nomad’s primary location, ensuring local compliance and reducing payroll friction. For many nomads, the EOR serves as their interface to payrolls, benefits, and other administrative aspects of HR. Prominent players in this space include Deel, G-P, and Papaya Global.

Travel and Living Platforms

Digital nomads often arrange for their housing and transportation needs on many of the same platforms as every other traveler. Digital nomads look to conventional travel platforms, OTAs, rideshare services, and the websites of “a la carte” service providers (e.g. coworking spaces, insurance) to pull together the resources they need.

While the current way of doing things might rely on disconnected systems, there is tremendous potential in the evolving digital nomad community market. Platforms such as nomads.com and Freaking Nomads aggregate resources in one spot while providing valuable information and crowdsourced guidance.

Digital nomads can no longer be considered edge cases. As the community continues to grow and its needs are better understood, Greenefield expects all-in-one marketplaces to grow in adoption and utility. This growth will rely on greater convergence between travel and fintech, as well as the development of more AI-enabled capabilities (e.g. tax estimation, intelligent compliance workflows, and predictive FX optimization).

Ultimately, this new mobility stack will collapse work, travel, payments, and identity into one experience layer.

Key Opportunities in the Future of Work, Finance and Travel

What does this mean for tech companies serving the digital nomad market? Advances in AI, FinTech, RegTech, and related areas set the stage for new products and delivery models to make the lives of digital nomads and other types of remote workers easier. Here are some areas to watch for innovation.

For fintechs, this is an opportunity to build portable financial infrastructure:

Multi-currency, multi-jurisdiction financial accounts. These help mobile workers hold, send, and spend money across countries without juggling separate bank accounts.

Income-based underwriting models. Where legal, these models allow lenders to approve credit on the basis of cash flow and quantified earning patterns, regardless of where the applicant lives or does business.

Cross-border credit and savings products. These are products that would make it easier for globally mobile users to build financial stability in their currency of choice, even when their income and residence change.

For EOR and payroll vendors, this is a chance to own the worker financial layer:

Embedded wallets with instant global payouts. This would let companies pay workers quickly in the currency that works best for them.

Built-in tax estimation and compliance. This refers to the automation of withholding, reporting, and cross-border obligations, for any cross-border employment scenario.

Automated benefits modularity. When an employee or contractor moves, benefits such as insurance adjust in turn.

For travel tech companies, this is a way to extend from booking into supporting the full mobility experience:

Integrated payments, insurance, and FX. This gives travelers and nomads a smoother experience by bundling the money layer into the booking or relocation flow.

Key Challenges

No discussion of fintech innovation can avoid the topics of regulation and compliance. Companies developing solutions for the digital nomad market must consider the following:

Regulatory fragmentation across countries. Financial products for mobile workers have to navigate different rules in every market, which makes scaling across borders slow and expensive.

Identity verification and KYC for individuals without fixed residency. When someone doesn’t have one permanent address, it becomes harder for platforms to verify identity and meet compliance requirements cleanly.

Tax complexity and lack of standardization. Mobile workers can trigger tax obligations in multiple countries, but there is no consistent global framework that makes reporting simple.

Data interoperability across platforms. Travel, payroll, banking, and tax systems often don’t share information well, so users end up re-entering the same data over and over.

Trust and risk management for mobile users. Because these users move frequently and operate across jurisdictions, platforms have to work harder to build trust and manage fraud, chargebacks, and compliance risk.

Conclusion: The Future of Finance and the Mobile Workforce

As work becomes increasingly detached from geography, financial infrastructure built around static residency and localized employment models will face growing pressure. Digital nomads may represent the earliest large-scale users of mobility-native finance, but they are unlikely to be the last.

The same expectations shaping the nomad economy — portability, flexibility, instant global payments, modular benefits, and seamless cross-border financial management — are gradually influencing remote employees, international contractors, fractional workers, and globally distributed companies alike.

This creates a major opportunity for fintech, people tech, payroll, insurance, and travel platforms willing to rethink how financial services are delivered in a world increasingly defined by mobility.

At Greenefield Consulting, we help innovative companies in fintech, future of work, and travel technology position themselves within emerging market shifts like borderless work and digital mobility. If you’re building products for digital nomads, remote workers, or globally mobile employees, Greenefield can help you define the right product narrative, positioning, and content strategy for this fast‑evolving market.